Banks

DRC: Rawbank, the successful model of family business!

Rawbank is a successful model of family business in DR Congo. His success story was discussed during the fifth edition of Makutano International Economic Forum in Kinshasa. Experts, businessmen, lawyers and executive of this bank reflected on Saturday, September 7, 2019, around the difficulties faced by family businesses face the challenge of sustainability.

The panellists have all started from a bitter conclusion: very often, the founders of family businesses have trouble passing the baton to successors. Five causes explain this difficulty. These are respectively:

Unpreparedness is often judged as a consequence of the egoism of founders. Also, in other cases, this preparation is happening in a hurry. Unlike companies whose founders are not African, children are introduced to business from an early age. They are oriented to follow courses of interest to the company. This is not the case for most Congolese in particular and Africans in general.

However, Rawbank which is a family business illustrates the case of a good preparation.

« In Rawbank, we saw Rawji’s children start at the bottom of the ladder and finish in positions of responsibility. This way of doing things allows the person promoted to understand the problems of each service, « said Deputy Director General for Risk and Administration Christian Kamanzi.

Then there are the inheritance rules from tradition. Very often, the panelists noted, positions of responsibility are attributed according to the birthright and not the skills.

They also talked about cultural pressure. If it is difficult to dissociate the entrepreneur from his person, there is an antagonism between the relationship and the passionate.

Added to this is the dispute over shares between children of a large family, they note. Which drives some to sell the business to third parties.

Finally, the expatriation of heirs. On this point, Joss Ilunga, CEO of Dijimba, shared his testimony. Living and working in Europe, he had to return home to take over the family business Pharmagros.

#Makutano5: table ronde autour du #family #business. @SultaniMakutano @tshiswaka5 @GoodLuck225 @AllegraFosh2 @AlainNdaba @SODEICO_ @Zoom_eco @waywebdigital @Widoobiz @Dan_Wawina @WeloAlex @MuzembeK @OnyumbeS @wembi_steve @FBNBankRDC @NyenyeziSolange @Rawbank_sa @qzafrica @ONU_fr pic.twitter.com/Tu0bKuoZdz

— mbesse ghislain (@ghislainmbesse) September 7, 2019

Experts believe that it is necessary to get around all these difficulties to sustain family businesses in the DRC. Starting from the example of the Rawji whose history goes back to the beginning of the XXth century when Merali Rawji (father of Mushtaque, Mazhar Aslam and Murtaza) settles in the east of what is then the Belgian Congo and begins the trade of the coffee and cocoa.

In 1966, the Rawji group acquired Beltexco, a consumer goods distributor. In 2002, Rawbank is launched in a chaotic banking sector. However, this does not shake the determination of Rawji to build the first commercial bank of the Congo.

With a constant and steady growth of its deposits ($ 1.5 billion, + 27% compared to 2017), credits ($ 665 million, + 59.5%) and total assets ($ 1.67 billion) of dollars, + 25%), Rawbank, in 2018, confirmed its leadership position and its willingness to think big for the Congo.

As much as it continues to expand its branch network across the country, Rawbank remains strongly committed to the people through a diversified and efficient program of corporate social responsibility. This program supports education, culture, health, supervision of children and vulnerable people.

As a reminder, this session of exchange and reflection of the fifth edition of Makutano was sponsored by Rawbank.

Nadine FULA

United Bank for Africa (UBA) DRC was represented at the fifth Forum Investing in Africa (FIA5) held from 10-12 September 2019 in Brazzaville, Republic of Congo. Its CEO, Patrick Kabisi, was the only panelist selected in the Congolese banking sector.

He intervened in the session on Human Capital Development as an analyst of the changing demographic and social environment.

Patrick Kabisi focused on areas where investment is needed, not only to close the gap in basic services, but also to help people become innovators, entrepreneurs, leaders and autonomous citizens, regardless of their income level.

These reflections also focused on opportunities for knowledge exchange and collaboration between African countries, China and the rest of the world on key institutional, regulatory and technological reforms.

Sub-Saharan Africa lags behind in most human capital indicators, and estimates show that the continent is only operating at 40% of its potential despite recent progress in health and education indicators.

At the same time, a skills gap hinders countries’ competitiveness in the global economy.

The objectives of the AIF5 were to examine how best to support economic diversification and job creation in African countries; to take stock of progress made and should chart the way forward.

Emilie MBOYO

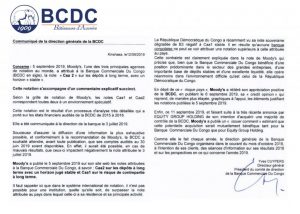

Despite the high country risk of DR Congo, Moody’s rating agency has just reiterated its positive assessment of the Banque commerciale du Congo (BCDC). In a publication relating to its « credit opinion » of 6 September 2019, it included in a more detailed manner the elements justifying Caa2’s ratings on long-term deposits with a stable horizon and Caa1 on long-term counterparty risk assigned to this Congolese bank.

« Banque commerciale du Congo enjoys a predominant position in the large corporate sector, a large stable deposit base and excellent liquidity, but operates in the difficult environment of the Democratic Republic of Congo, » said Yves Cuypers, BCDC’s Executive Director in a statement to Zoom Eco.

Indeed, it is not possible for a banking institution, in the international rating system, to exceed the rating assigned to the country in which it has its residence and main activity. Congo DR has recently seen its sovereign rating downgraded from B3 negative to Caa1 stable.

#RDC : Moody’s attribue à la @BCDC_RDC la note « Caa2 » sur les dépôts à long terme | via @Zoom_eco– https://t.co/ecwGqxNIcR

— Zoom Eco (@Zoom_eco) September 13, 2019

Logically, it follows that no Congolese bank can be assigned a higher rating than that assigned to DR Congo. What is more normal than BCDC’s Caa1 rating means that the bonds are speculative and subject to high credit risk.

However, BCDC’s efforts are acknowledged by Moody’s, which welcomes the announced acquisition of a majority stake in BCDC by the Equity Group.

« Moody’s has published an (issuer comment) considering that this potential acquisition would be mutually beneficial for both the Banque commerciale du Congo and Equity Group Holding, » insisted Yves Cuypers.

Eric TSHIKUMA

Moody’s, one of the world’s leading rating agencies, has assigned two ratings to the Banque commerciale du Congo (BCDC). These are Caa2 on long-term deposits with a stable horizon and Caa1 on long-term counterparty risk. According to an official statement from the bank, these two ratings correspond to a speculative environment. Below, the details:

-

breaking news5 ans ago

breaking news5 ans agoDRC: dam Zongo II, a project poorly evaluated technically and financially (study)

-

breaking news5 ans ago

breaking news5 ans agoDRC: International Banker Awards SOFIBANQUE Two 2019 Best Bank Awards

-

breaking news5 ans ago

breaking news5 ans agoDRC: Government incorporates IDEF into the cost of airfare

-

Banks5 ans ago

Banks5 ans agoDRC: Equity Bank strengthens its partnership with VISA inc.

-

breaking news5 ans ago

breaking news5 ans agoDRC: Dandy Matata calls for a state of emergency in the education sector

-

breaking news5 ans ago

breaking news5 ans agoDRC: DIVO launches renovations to the Tata Raphael stadium

-

breaking news5 ans ago

breaking news5 ans agoDRC: ACERD expects renewable energy investment opportunities

-

breaking news5 ans ago

breaking news5 ans agoDRC: Kangudia launches Fiscal Year 2020 Budget Orientation Seminar